Equal Housing Lender

Down Payment Assistance for Clients (DPA)

HUD and Fannie Mae/Freddie Mac Qualifying Income Levels for Down Payment Assistance Differs!

Links to Income Levels, Differences and How to Calculate Above 100% Income Levels

Check Income Levels for Down Payment Assistance Programs Upfront!

Links to Income Levels

- HUD Income Limit: https://www.huduser.gov/portal/datasets/il.html#2022

- Fannie Mae Area Median Income Lookup Tool: https://ami-lookup-tool.fanniemae.com/amilookuptool/

- Freddie Mac NEW Area Median Income and Property Eligibility Tool: https://sf.freddiemac.com/working-with-us/affordable-lending/area-median-income-and-property-eligibility-tool

Differences in Income Calculations

- HUD Income Limit levels for 50% and 80% are not the same as Fannie Mae/Freddie Mac 50% and 80% Area Median Income (AMI) levels.

- HUD Income Limits are based off of family size. Fannie Mae/Freddie Mac AMI is based on income of qualifying borrower(s), not family size.

- Fannie Mae 80% AMI is maximum income for Home Ready Affordable product.

- Freddie Mac 80% AMI is maximum income for Home Possible Affordable product.

Income Levels at 100% and Above

- HUD: locate Median Family Income (100%) for state/county on HUD Income Limit levels.

- Fannie Mae: locate 100% Area Median Income on Area Median Income Lookup Tool.

- Freddie Mac: locate 100% Area Median Income and higher on NEW Freddie Mac Area Median Income and Property Eligibility Tool

How to Calculate Income Levels Above 100% for All Mortgage Types Above

- For 115% Income: Multiply 100% income x 115%

- For 120% Income: Multiply 100% income x 120%

- For 140% Income: Multiply 100% income x 140%

For 160% Income: Multiply 100% income x 160%New Paragraph

DPA Program Frequently Asked Questions

Please let us know when you hear of new programs across the U.S. by emailing clients2homeowners@gmail.com.

DPA Articles to Help MLOs

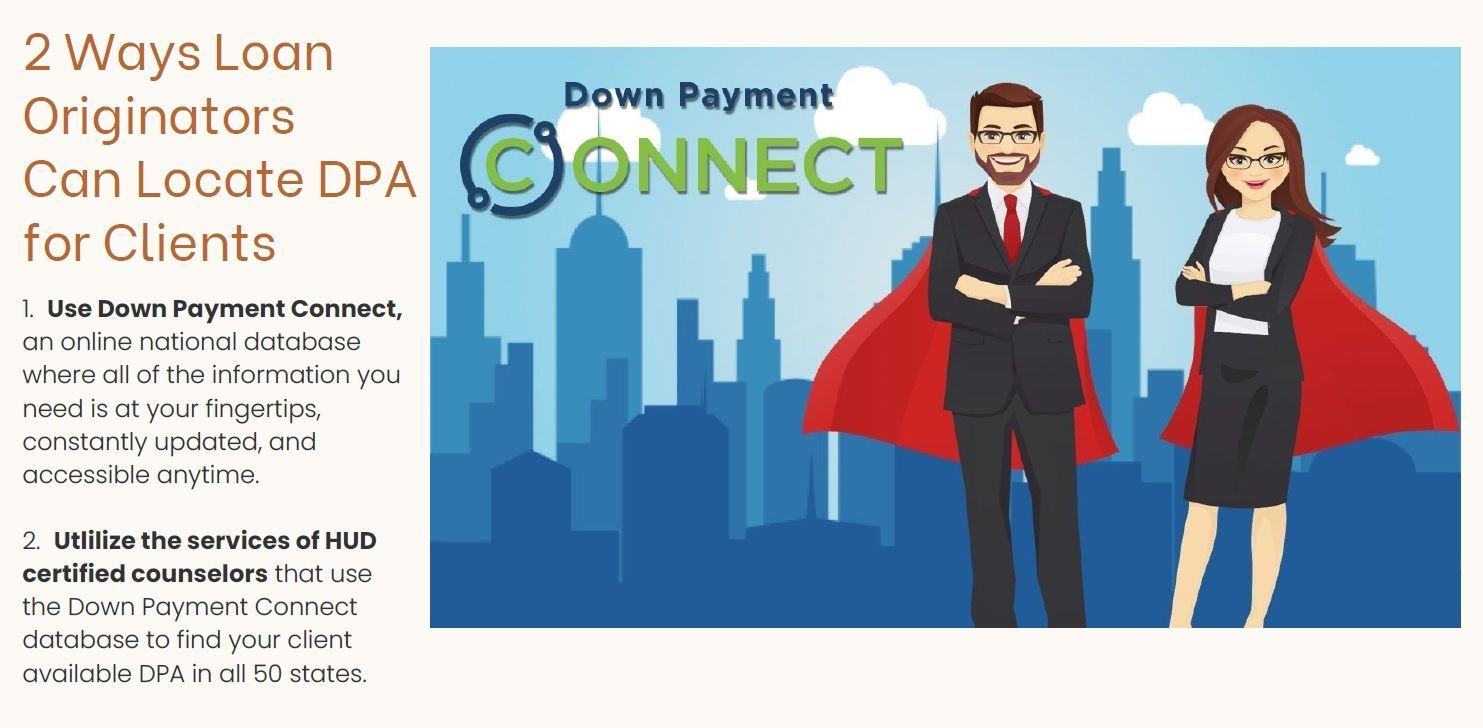

Down Payment Connect is already being used by MLOs and Realtors. Now it's available to HUD Counselors through HomePrep! Down payment assistance is quickly rising to the top need for clients wishing to purchase a home. Down Payment Connect , the back-end data provider for the parent Downpaymentresource.com , houses every down payment assistance program in the US and provides extremely detailed information laid out in a consistent format for each DPA program in their system. Throughout the last two years, Downpaymentresource.com administrators have worked with MLO’s and the HomePrep developers to add nearly all wholesale down payment assistance programs to their platform and they didn't stop there! Extensive filters that allow for selection of specific client needs such as type (ie. SFR, manufactured homes, condos, multi-family, ADU’s), uses like renovation, above AMI income levels, non-1st time homebuyers are just a few of the filters you will find along with stand alone 2nd mortgages, combined 1st and 2nd mortgages and grants. DownpaymentResource.com is also in many MLS systems across the US and provides limited directory information and a free landing page for realtors to promote that they use DPA. Both MLO’s and realtors can subscribe to Down Payment Connect to get more of the extensive directory and back-end tools. Now, through HomePrep, HUD counselors can also use the Down Payment Connect system to filter trhough DPA programs that clients are qualified for, and can even provide wholesale programs when working with an independent loan originator (often called a mortgage broker)! Through HomePrep, HUD counselors are now able to provide MLO’s and clients with the DPA programs that they have found the client is eligible for.

Clients2Homeowners.com makes a pivot!

Mortgage Loan Originators, Realtors and HUD Housing Counselors Who Need to Find and Promote Down Payment Assistance (DPA) to Clients Need this Tool!

Here’s How to Organize DPA for Your Area and Start Selling!

Pam Marron, NMLS# 246438

Innovative Mortgage Services, Inc. NMLS# 250769