Equal Housing Lender

Student Loan Help for Clients Using HomePrep

Loan originators can offer Student Debt Solutions (SDS) as an "MLO DIY Solution" for clients OR utilize HUD counselors that use SDS through HomePrep! HomePrep!

Click here to view video.

Loan originators working with clients who have student loans are facing new credit challenges and payment constraints that may impact a prospective homebuyer’s ability to qualify for a mortgage. Understanding these issues and the available solutions can help MLOs better guide their clients through the home financing process.

How to Use Student Debt Solutions

MLO DIY Solution

MLO's can refer clients directly to Student Debt Solutions for repayment plans and default resolution. There is no cost to go all the way through to seeing plans client is eligible for! A cost is only incurred if the client would like to implement a new plan through SDS.

HomePrep for MLOs

Student Debt Solutions is also available for clients that go through HomePrep.

Note: a special discount is already applied for clients through MLO DIY Solutions or HomePrep for MLOs.

Disclaimer: Ms. Marron, Clients2Homeowners.com website developer, receives no compensation for the SDS service or any other services promoted on this site.

Click on flyer for SDS:The Essential Tool for Loan Officers

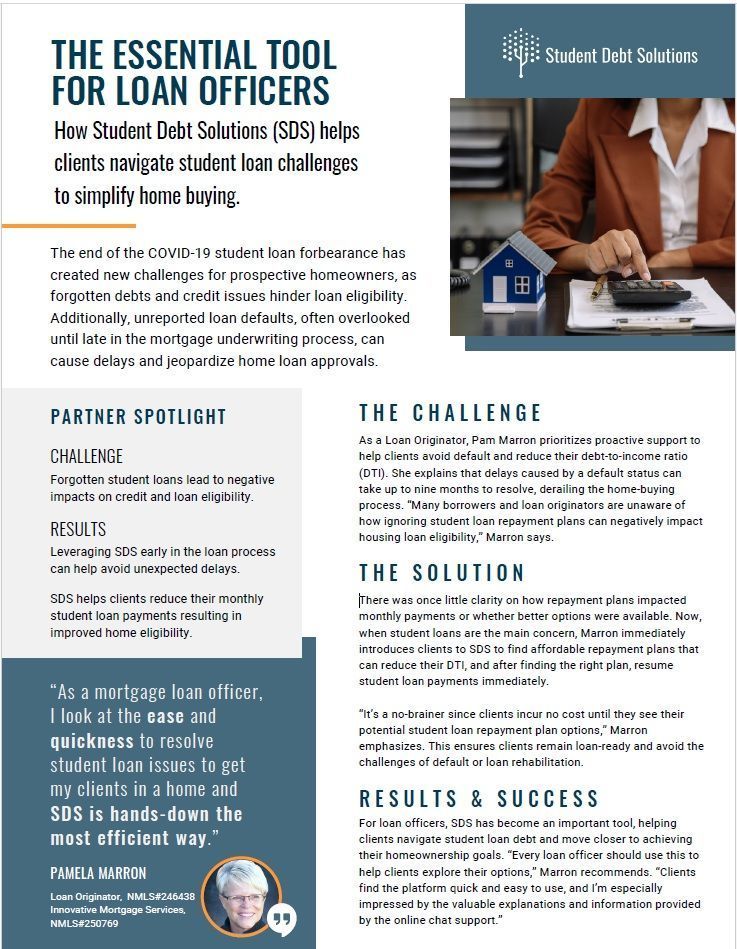

Loan Originator Recommendation

For loan originators who have clients with student loans, whether federal or private, this program gives options that may decrease a student loan payment and increase buying power to purchase a home, or even escalate a payment to pay student loan debt off early.

Student Debt Solutions:

- provides details of all federal programs that the client is eligible for and is FREE to view. Client only pays if they want SDS to assist them to sign up for a plan.

- compares the savings of a current student loan payment to a new repayment plan.

- Has outstanding support!

- can provide a refinance of private student loans.

- offers defaulted student loan solutions.

Disclaimer: Pamela Marron, Licensed Loan Originator, NMLS#246438 , receives no compensation from any services shown on Clients2Homeowners.com. Student Debt Solutions was analyzed with other student loan repayment plan programs that will be linked at the bottom of this page.

Unlock Your client's Homeownership Dreams

Student Debt Solutions: A DIY Solution for Mortgage Clients with Student Loans

2 Options for MLO's to Use for Clients Who Need Help With Student Loan Repayment Plans and Solutions for Defaults!

1. SDS is a DIY Solution for Clients

Who Need Student Loan Help

If your client has federal student loans and is not already set up with a repayment plan, there is a federal government resource at Studentaid.gov.

Or, your client can go to Student Debt Solutions (SDS) and get a list of all plans available to them for FREE by answering a short list of questions.

This is a good resource for a client:

- that only needs help with a student loan repayment plan or student loan default solution to get a mortgage.

- whether they need a purchase or refinance mortgage.

2. SDS is also used by HomePrep, Where MLOs and their Clients Connect to a HUD Counselor!

Looking to refer your clients with issues preventing them from proceeding with a mortgage to a professional trained to get the client mortgage ready? Consider using HomePrep that connects the MLO and client to a HUD counselor that can provide and follow up with your client for Student Loan help using Student Debt Solutions (SDS) and a number of other services provided through HomePrep!

When the client is ready for a mortgage, you are notified!

Understanding Mortgage Underwriting Guidelines

Navigating the complexities of mortgage underwriting can be challenging. Here’s a breakdown of the guidelines for FHA, Fannie Mae, Freddie Mac, VA, and USDA loans, especially in various payment scenarios.

Fannie Mae Guidelines

Freddie Mac Guidelines

FHA Guidelines

VA Guidelines

USDA Guidelines

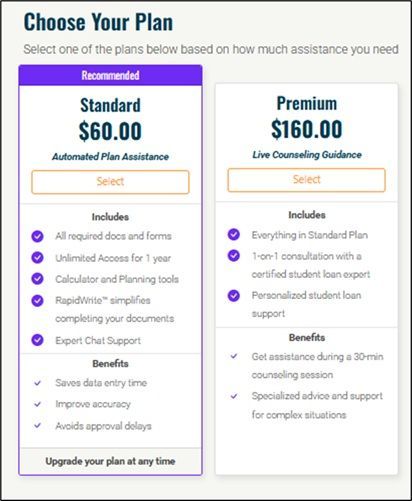

SDS Costs

Student Debt Solutions

Payment is only needed for applying for your Plan.

Standard: $60

- Required Forms

- Instructions

- Automation Tools

- Expert Chat Service

Premium: $160

- All of the Above

- Live Counseling Session

Student Loan Articles

90-day student loan delinquencies are silently crushing credit scores and killing mortgage approvals. Here’s how MLOs can fight back.

A Few Extra Points MLOs Need to Know For Clients With Student Loans

MLOs: Review 7 Points Before Pre-Approving Clients with Student Loans

Questions answered about student loan repayment plans, default and more.