Equal Housing Lender

MLOs: Review 7 Points Before Pre-Approving Clients with Student Loans

Pam Marron, Licensed Loan Originator, NMLS# 246438 • April 8, 2025

MLOs: Review 7 Points Before Pre-Approving Clients with Student Loans

Investigate these 7 points BEFORE giving a client with student loans a Pre-Approval letter for a mortgage.

1. Retrieve a Complete Student Loan Payment History Letter

When reviewing the credit report of a client who has student loans, you may find that the most currently serviced student loan may not show up on the credit report, and a previously serviced student loan will. Have your client contact their current servicer and retrieve a complete payment history letter with a payment noted and that is up to date. If your clients’ loans were transferred from a different servicer within the last 24 months, make sure your client retrieves a payment history letter from that servicer as well.

Directions for how to retrieve this information for federal student loans can be found at Studentaid.govat “How can I see my federal student loan payment history?”

Separately, Federal Student Loan Updates provides where previous servicers have transferred to if this is unknown.

Getting the complete payment history is especially important if the client has delinquent payments in their student loan payment history. Student loan default starts at 270 days, which equates to 9 months.

2. Get Written Proof of the Current Student Loan Payment

Make sure that the client gets a letter from their servicer that provides a minimum monthly payment amount. Having a $0 monthly payment will require that the loan originator count a minimum percentage of the full loan balance as the client’s student loan debt. And if the student loan still shows in “forbearance”, an automatic 1% of the balance is the required payment that loan originators need to insert for student loan debt.

Most often, the minimum required payment can be calculated by the servicer and is usually lower than the percentage dollar amount required for each mortgage loan type.

3. Run client’s loan application through both Fannie Mae Desktop and Freddie Mac Loan Product Advisor automated underwriting systems (AUS) for an Approval before issuing a pre-approval letter.

The Fannie Mae and Freddie Mac AUS systems pick up back-end credit that may not be visible on a mortgage credit report.

a. Run the clients file through both Fannie Mae and Freddie Mac automated systems. Go to Findings and check Credit for any directions related to student loan accounts and follow them. Compare credit detail addressed in the AUS findings to your credit report.

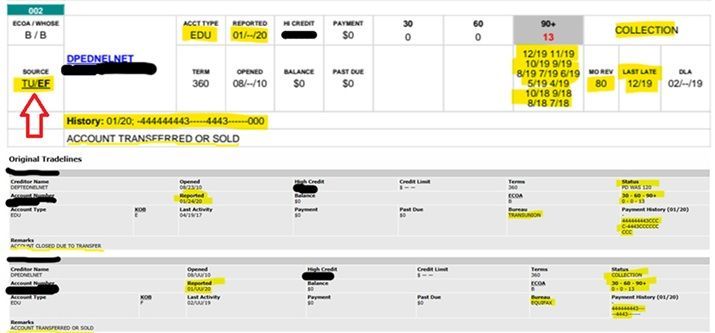

b. If there are late payments and you’re not sure which of the credit bureaus reported the late payment dates, detailed credit history for each bureau of TransUnion, Equifax and Experian can be seen on credit reports that are provided through Meridian Link. (Not all credit reporting agencies use the Meridian Link platform.) This applies to both soft and hard-pull credit reports and Meridian Link is on both reports if your credit reporting agency uses them.

The credit report at the bottom of this page shows where you may find the Meridian Link on your credit report for the 2 credit bureaus, Trans Union and Equifax, that are shown.

4. Check CAIVRS UPFRONT to Make Sure a Client's Federal Student Loan is Not Prohibiting Them from Getting an FHA, VA or USDA Mortgage.

Get your client cleared through the CAIVRS system upfront! CAIVRS is a database used by federal agencies to identify individuals who are delinquent or in default on federal debts, including student loans. A CAIVRS alert can prohibit your client from proceeding with an FHA, VA or USDA loan. There are solutions for delinquency and default. However, having adequate time to resolve these issues is needed.

I spoke with a Sr. HUD Underwriter at the HUD Resource Center on 3/24/2025 who then sent a response via email. Regarding CAIVRS, we should check public records and credit information through CAIVRS UPFRONT to verify that the Borrower is not presently delinquent on any Federal Debt.

5. Let Clients and Their Realtor Know Not to Actively Seek a Home Purchase Until a Loan Repayment Plan Has Been Fully Approved!

If your client has recently applied for a student loan repayment plan, make sure your client and their realtor are not actively looking for a home. The wait-timeframe for this service is currently 30 to 60 days. Consider having the client use the Student Debt Solutions platform (SDS) that shows all repayment plans available and will go all the way through selecting a plan allowing you, the MLO, to see what payment the client could realize. This is FREE and SDS only charges if the client wishes to proceed with an application for the desired plan.

6. Make Sure Your Client IS or GETS CURRENT on Their Student Loan Payment!

Make sure your client stays current on their student loan, and if they aren’t, getting current needs to be their priority! We’ve already seen credit scores drop dramatically due to delinquent student loan credit. And default solutions will stall your client from getting a mortgage for 6 to 9 months AFTER getting a default payment option in place.

7. Make Sure Your Client Recertifies Income With Their Student Loan Servicer by the Deadline They’ve Been Provided!

If your client misses the recertification deadline for their income-driven repayment (IDR) plan, they’ll be removed from the plan and placed on an alternative repayment plan, likely with a fixed monthly payment amount, and potentially higher payments.

When MLOs pro-actively take the time to go over these points with clients who have student loans and who desire to purchase or refinance a home, your clients will view you as a trusted resource. Checking these steps upfront allows us an opportunity to assist our clients and avoid pitfalls, like having to do a Rapid Rescore mid-contract that we MLO’s have to pay for. Let’s get in front of this, MLO's!

Go to DIY Student Loan Help for Clients at Clients2Homeowners.com for more.

Article author Pamela Marron is a licensed loan originator (NMLS#246438) who made Clients2Homeowners.com as a resource for mortgage loan originators to assist clients with challenges that may prevent them from obtaining a mortgage. Ms. Marron receives no compensation from any services mentioned in this article or on the website Clients2Homeowners.com.

The red arrow below shows where Meridian Link is accessible on the credit report. In the gray box that shows

90+, 13 months of lates show up. This account could be a defaulted student loan already as default starts at 270 days, or 9 months.

A Few Extra Points MLOs Need to Know For Clients With Student Loans

Questions answered about student loan repayment plans, default and more.

Update: Effective March 26th, 2025, IDR Processing is Available Again!