Equal Housing Lender

Other Resources

Partner with Housing Counselors and Certified Credit Counselors at HUD Agencies

Housing Counseling is independent, expert advice customized to the need of the consumer to address the consumer’s housing barriers and to help achieve their housing goals and must include the following processes: intake; financial and housing affordability analysis; an action plan, except for reverse mortgage counseling; and a reasonable effort to have follow-up communication with the client when possible.

The content and process of housing counseling must meet the standards outlined in 24 CFR part 214. Homeownership counseling and rental counseling are types of Housing Counseling.

HUD Certified Credit Counselor FAQs

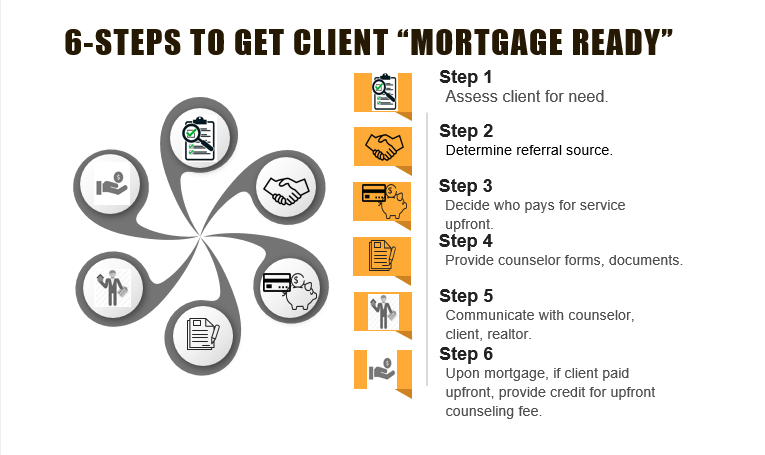

Steps for Loan Originators to Refer Clients to Housing Counseling Agency (HCA)

Explaining Fee for Service Payment

U.S. Department of Housing and Urban Development

Office of Housing Counseling | Model Funding Agreements and Fee Structures

Housing counseling agencies (HCAs) acquire funding in numerous ways, including being paid a fee for the services they provide. The fees can be paid by clients (with the exception of Foreclosure Prevention and Homeless counseling clients), non-profit partner agencies, and private sector partners. The fees provided to the HCA can vary depending on the services being provided. This guide provides information about the basic components in a funding agreement.

Subcontracting (under Foreclosure Counseling Fee Structures)

The next most common funding models are focused within the sub-contracting model of funding. This funding model involves an HCA subcontracting with a mortgage investor to complete a statement of work including provision of counseling services to the investor’s portfolio of borrowers. This funding model is based on a fee for service model, wherein the HCA receives either a payment for services rendered or payment based on a set of prescribed outcomes. In many cases a base fee for service is provided with an incentive payment for a borrower’s resumed steady payment history. This fee structure is generally designed to provide the housing counseling agency with a payment between $300 and $1,000 per client to complete work related to resolving the mortgage delinquency on behalf of the mortgage investor.

Pre-Purchase Counseling Fee Structures Lender Paid

Pre-purchase counseling provides mortgage lenders with educated and confident customers, which can make the application process proceed more smoothly, with fewer surprises and a higher chance for high performance across the life of the mortgage loan. The investment into pre-purchase housing counseling is likely to return a greater profit margin than those who choose to not promote and invest into pre-purchase counseling.

Homeownership Counseling

The most common form of fee for service within pre-purchase counseling is the payment of a fee by a mortgage lender to an HCA for counseling prospective borrowers about the pro and cons of homeownership. In many cases this payment is irrespective of whether the client chooses to proceed with a loan closing.

Pre-purchase Counseling

In other cases the mortgage lender has defined pre-purchase counseling as an underwriting requirement that must be completed prior to a loan closing. The fees paid by a mortgage lender can range from $25 for a customer’s attendance at a homeownership education workshop, to a payment of $500 for a combination of pre-purchase counseling and post-purchase education. In some cases a mortgage insurance company or other party with a financial interest in the transaction will invest in this service.

Down Payment Assistance Counseling

Many down payment assistance programs have a pre-purchase counseling/ education requirement. In many cases a down payment assistance program will pay for the cost of pre-purchase counseling services.

Define Strict Conflict Of Interest Statements And Disclosures

In any funding model, it is important to define strict conflict of interest statements and disclosures to avoid even the appearance of a conflict of interest. When developing a fee structure for a pre-purchase counseling program, it is very important to avoid a fee structure where an HCA’s compensation is based on the terms, conditions, or size of a mortgage loan transaction. See the HUD Housing Counseling Handbook for both conflict of interest guidance as well as steps to avoid lender steering issues. Once an HCA decides to enter into a relationship with a lender, HUD requires that the HCA enter into a Memorandum of Understanding (MOU), signed by both parties, to formalize the relationship. This MOU must state that:

- The client will choose between comparable products from at least three different lenders.

- The fee income is based on services rendered, NOT on the amount of the loan.

Client Paid

Charging a client for pre-purchase counseling is an effective manner in which to engage the client in the counseling process. By charging a fee for pre-purchase counseling a client is more invested in the process of learning. While HUD requires any client based fees to allow for a hardship waiver, it is acceptable and commonly practiced to charge clients for pre-purchase counseling.

CFPB Issues Policies to Facilitate Compliance and Promote Innovation | First No-Action Letter Issued to HUD Housing Counseling Agencies | SEP 10, 2019

WASHINGTON, D.C. – The Consumer Financial Protection Bureau (Bureau) today issued three new policies to promote innovation and facilitate compliance: the No-Action Letter (NAL) Policy, Trial Disclosure Program (TDP) Policy, and Compliance Assistance Sandbox (CAS) Policy. The Bureau proposed the policies in 2018 and received public comments on each from a diverse array of stakeholders.

Regulatory uncertainty can hinder the development of innovative products and services that benefit consumers. NALs provide increased regulatory certainty through a statement that the Bureau will not bring a supervisory or enforcement action against a company for providing a product or service under certain facts and circumstances. The new NAL Policy improves on the Bureau’s 2016 NAL Policy by having, among other things, a more streamlined review process focusing on the consumer benefits and risks of the product or service in question.

The Bureau today issued its first NAL under the new NAL Policy in response to a request by the Department of Housing and Urban Development (HUD) on behalf of more than 1,600 housing counseling agencies (HCAs) that participate in HUD’s housing counseling program. In 2018, HUD brought concerns to the Bureau about HCAs and lenders not entering into agreements that would fund counseling services due to uncertainty about the application of the Real Estate Settlement Procedures Act (RESPA). Expressing similar concerns, the Coalition of HUD Intermediaries filed a comment letter in February 2019 noting the insufficiency of the Bureau’s old NAL Policy and supporting the new NAL proposed policy. The no-action letter essentially states that the Bureau will not take supervisory or enforcement action under RESPA against HUD-certified HCAs that have entered into certain fee-for-service arrangements with lenders for pre-purchase housing counseling services. The NAL, which is an exercise of the Bureau’s supervisory and enforcement discretion, is intended to facilitate HCAs entering into such agreements with lenders and will enhance the ability of housing counseling agencies to obtain funding from additional sources.

Under the new TDP Policy, entities seeking to improve consumer disclosures may conduct in-market testing of alternative disclosures for a limited time upon permission by the Bureau. The Dodd-Frank Act gives the Bureau the authority to provide certain legal protections for entities to conduct trial disclosure programs, as outlined in the TDP Policy. The new policy streamlines the application and review process.

The CAS Policy enables testing of a financial product or service where there is regulatory uncertainty. After the Bureau evaluates the product or service for compliance with relevant law, an approved applicant that complies in good faith with the terms of the approval will have a “safe harbor” from liability for specified conduct during the testing period. Approvals under the CAS Policy will provide protection from liability under the Truth in Lending Act, the Electronic Fund Transfer Act, or the Equal Credit Opportunity Act.

“Innovation drives competition, which can lower prices and offer consumers more and better products and services. New products and services can expand financial options, especially to unbanked and underbanked households, giving more consumers access to the benefits of the financial system. The three policies we are announcing today are common-sense policies that will foster innovation that ultimately benefits consumers.” said Consumer Financial Protection Bureau Director Kathleen L. Kraninger.

Down Payment Connect

For Loan Originators and Real Estate Agents

Start new homebuyer conversations with your personalized landing page

Today’s consumers are spending more time online getting prepared for homeownership and researching their down payment options. Now is the time to show them you can help.

We know it’s difficult to show homebuyers up-to-date down payment program opportunities. We created a better way.

Down Payment Connect makes it easy to match buyers to down payment help that is right for them. We track the details for more than 2,400 homeownership programs across the country, including all the options right in your backyard.

Here’s how it works:

- You promote your personalized landing page anywhere you are online.

- Buyers search for programs through your landing page.

- Buyers view basic results and complete the contact form to get more details.

- You get leads delivered to your inbox with details about all their results.