Equal Housing Lender

2.DIY Credit: Short Term

Short term credit help is defined as 1 to 6 months of help before the client’s credit is acceptable for the best mortgage they qualify for.

MLO DIY is most often short-term credit help.

Using CreditXpert

1. Credit Score Simulation & Improvement

CreditXpert analyzes credit data and simulates different actions—like paying down balances or removing inaccuracies—to show how those changes could impact the borrower’s credit score.

CreditXpert provides actionable, time-sensitive plans (e.g., “Pay down this credit card by $500 to increase your score by 15 points”).

This allows borrowers to make targeted moves before their credit is re-pulled, often in just a few days or weeks.

By addressing credit issues early and clearly, delays due to credit concerns can be avoided.

CreditXpert is available to MLO’s either through a

subscription or through your credit reporting agency.

Using Meridian Link

Meridian Link shows is part of the credit report if your credit reporting agency includes it. This platform breaks out each of the 3 credit bureaus, (Experian, Trans Union and Equifax) for each creditor enabling the viewer to pinpoint which credit bureau may be providing negative or no information on each creditor tradeline.

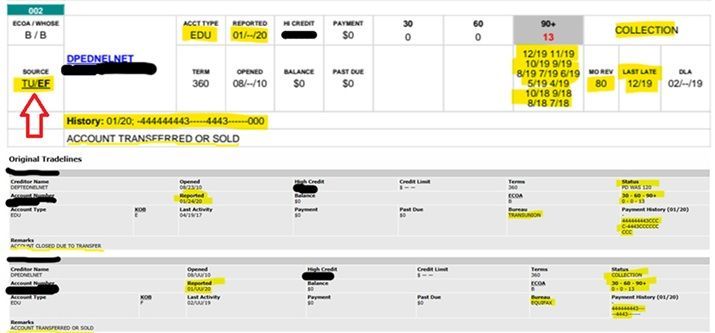

When Innacurate Credit Exists on the Credit Report, Use 5 FNMA Codes in Desktop Originator

There are correction codes that can be used for short sales disclised as a FCL and other erroneous credit. Click here for more details.

7 Steps to Review for Clients with Student Loans

Click here to find out 7 Things to review for clients that have student loans that may have delinquencies or are in default.

Avoid Rapid Rescores during Loan Process-Do AUS Run Upfront!

If there is any question about a clients credit, MLOs should run the client xml file through the Fannie Mae and/or Freddie Mac automated underwriting system (AUS) before giving the client the go-ahead to start looking for a home. Both AUS systems can pick up credit that may not be visible on the face of a credit report. It's expensive and nerve-wracking dealing with a credit issue where detail isn't apparent on credit, especially during a contract timeframe. Remember, you the MLO, must pay for the Rapid Rescore.

Check Credit & Liabilities in AUS for Dispute Direction

Click here to see how to check on Disputes with CreditXpert when brought up in Fannie Mae and Freddie Mac AUS findings.