Equal Housing Lender

Mortgage Credit Score vs Consumer Credit Score

By Kim Pinelli for CreditXpert | May 6, 2024 • March 28, 2025

The blog below explains the difference between mortgage credit scores and consumer credit scores.

Mortgage lenders use a FICO score, which is different from the Vantage 3.0 consumer credit score that individuals may access through services like Credit Karma.

Key points:

Mortgage Credit Score (FICO): Used by over 90% of mortgage lenders and emphasizes payment history (35%), credit utilization (30%), credit length (15%), credit mix (10%), and inquiries (10%). Scores range from 300 to 850.

Consumer Credit Score (Vantage 3.0): Emphasizes payment history (40%), age and type of credit (21%), credit utilization (20%), balances (11%), recent credit (5%), and available credit (3%).

Payment History: It’s crucial for both scoring models, and late payments can negatively impact the score.

Credit Utilization: It’s important for both but holds more weight in the FICO score.

Differences: The consumer credit score also considers balances and available credit, while the FICO score places a heavier emphasis on credit mix and length.

Now, onto the good stuff…

If you’ve ever applied for a mortgage only to find out that the credit score the lender sees is much different than what you’ve found pulling your credit scores from Experian or your credit card services, you aren’t alone.

Mortgage lenders use a different credit scoring model than consumers have access to, which means they may see a different credit score than what you expect.

Here’s how they differ.

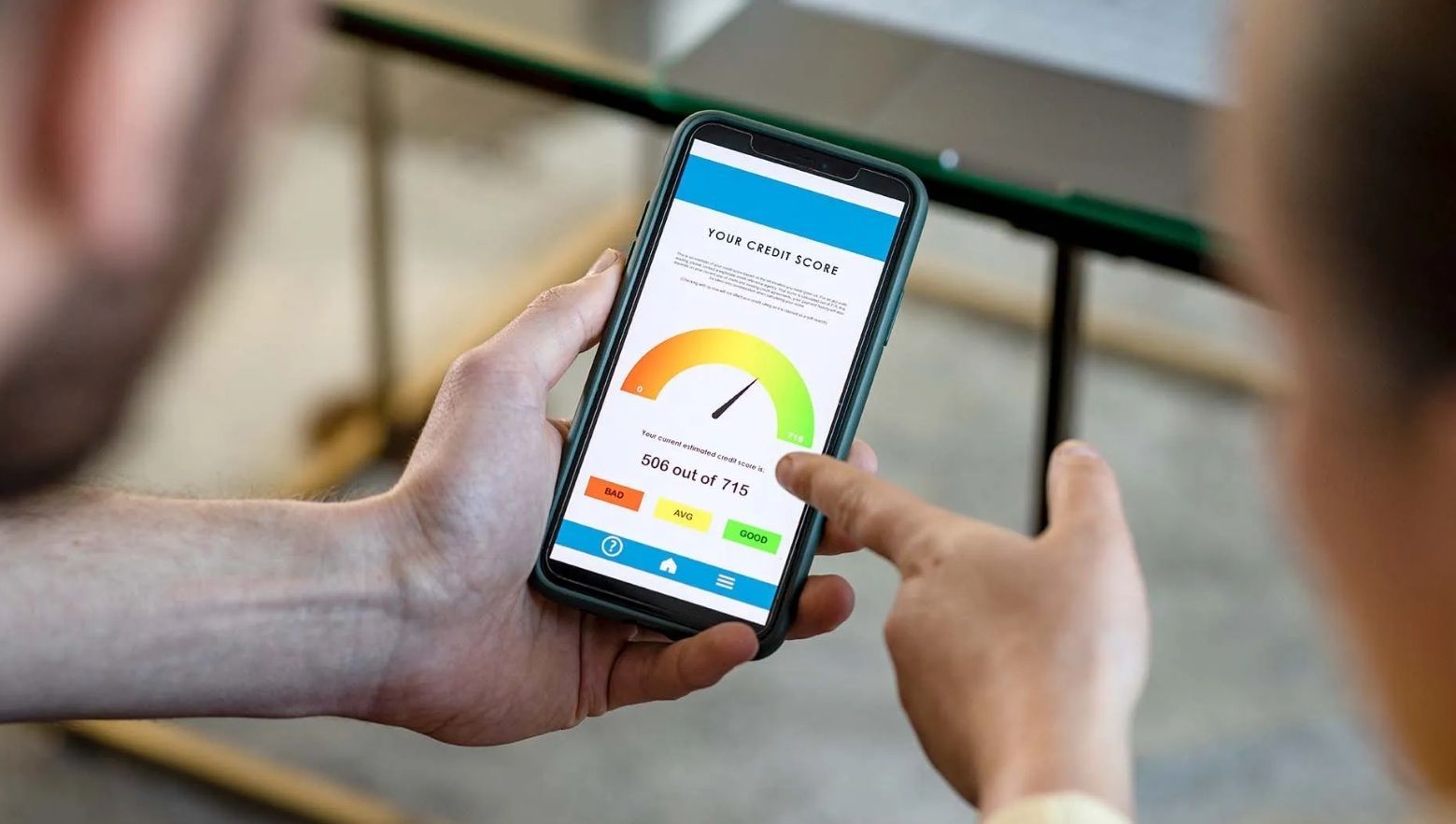

What is a Mortgage Credit Score?

Your mortgage credit score is likely FICO, a score created by Fair Isaac and Company. Over 90% of mortgage lenders use this credit scoring model from all three credit bureaus – Trans Union, Equifax, and Experian.

The credit scores range from 300 – 850 with 850 being the highest score.

How are Mortgage Credit Scores Calculated?

Mortgage credit scores put a lot of emphasis on payment history and credit utilization with other factors playing a role too.

- 35% payment history – Your payment history tracks how well you make your payments. Any payment made 30 days or more past the due date hurts your credit score, whereas a timely payment history can greatly improve your credit score.

- 30% credit utilization – Your credit utilization is a comparison of your total outstanding debt compared to your credit lines. For example, if you have a $1,000 credit line and you have $500 outstanding, you have a 50% credit utilization rate. Ideally, you should keep your credit utilization rate lower than 30% for the best results.

- 15% credit length – The age of your credit affects your credit score too. The ‘older’ your credit is, the better it is for your credit score. Don’t close old accounts unless it’s absolutely necessary as this is an easy way to increase your credit score.

- 10% credit mix – Lenders like to see that you can handle a variety of debt including credit cards (revolving debt) and installment debt (mortgage loans, personal loans, car loans, etc.)

- 10% inquiries – Each time you apply for new credit or take out new credit, it slightly influences your credit score.

What is a Consumer Credit Score?

Consumer credit scores are the scores you see when you use services like Credit Karma or check your credit score provided by your credit card company or bank.

Consumer credit scores use the Vantage 3.0 scoring model, which as you’ll see below uses different factors.

- 40% payment history – Your payment history is extremely influential in your consumer credit score, just as it is with your FICO score.

- 21% age and type of credit – Next is your credit history length and type of credit, which is a combination of your credit length and credit mix with a FICO score.

- 20% credit utilization – Your credit utilization rate doesn’t affect your credit score as much as it does with a FICO score, but it still plays an impactful role.

- 11% balances – Higher balances, especially credit card balances, can hurt your credit score as lenders like to see lower balances for a lower risk of default.

- 5% recent credit – Your recent credit activity including opening new accounts or even just applying for new credit can affect your future financial capabilities.

- 3% available credit – It doesn’t have a large impact on your credit score but having too much available credit could show that you take out any credit that’s available to you even if you don’t need it.

To learn more about how CreditXpert can help borrowers and for a mortgage credit calculator, click here.

The Major Differences

As you can see, your payment history plays the largest role in both your mortgage and consumer credit score. You must make your payments on time. From there, the differences begin with credit utilization a major factor in lenders’ decisions since too much outstanding debt can make it hard to afford a new mortgage.

Mortgage credit scores focus mainly on your payment history, credit utilization, and credit mix. This is how they determine you are a good risk and could afford the mortgage payment you’re applying for.

Final Thoughts

Even if you have a good consumer credit score, don’t assume your mortgage credit score will be the same. Work with your lender to raise your mortgage credit score using CreditXpert – achieve more purchase power and a lower interest rate.

You may also want to take care of any collections as quickly as possible as depending on the FICO model lenders use, collections may get included in your score, even if you’ve paid them. The more time in between when they’re paid and when a mortgage lender pulls your credit though, the better it will be for your credit score.

Sources: https://www.forbes.com/advisor/credit-score/what-is-vantagescore/, https://www.investopedia.com/financial-edge/0212/how-is-fico-calculated.aspx

From CreditXpert website.

A Few Extra Points MLOs Need to Know For Clients With Student Loans

MLOs: Review 7 Points Before Pre-Approving Clients with Student Loans

Questions answered about student loan repayment plans, default and more.